The Continuing Evolution of Carbon and Energy Management Software

<p>As more and more companies adopt comprehensive software suites to manage their energy and greenhouse gas emissions, there are three market segments with widely different needs, instead of just one -- and plenty of solution providers to meet those needs.</p>

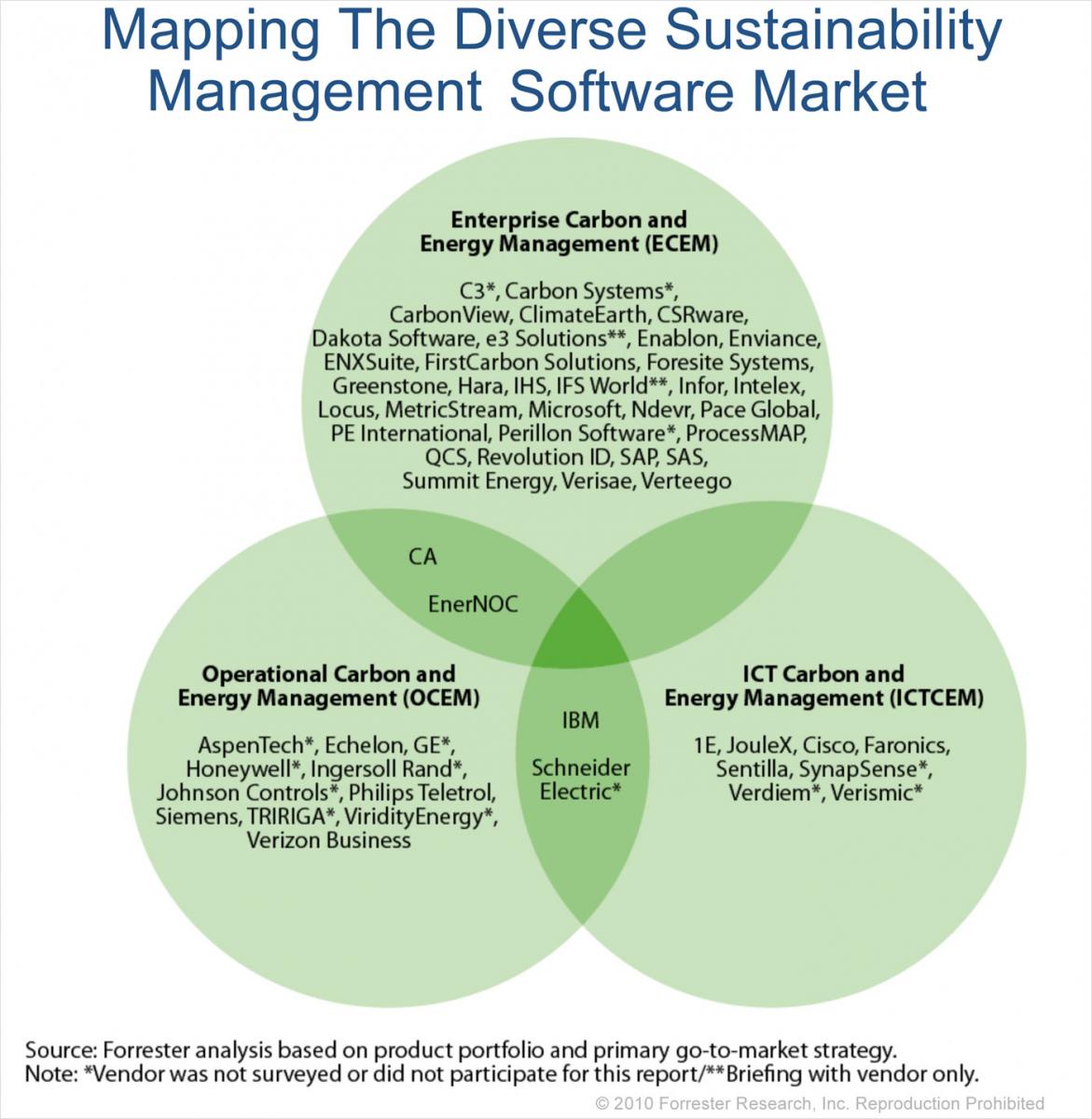

My colleague Daniel Krauss and I are putting the finishing touches on a comprehensive research report on the current state and future prospects for enterprise carbon and energy management (ECEM) software. We surveyed more than 40 suppliers, did interviews and demos with more than 20, and drew upon our ongoing discussions with consultants, service providers, and of course enterprise buyers that are participating in the takeoff phase of the ECEM market. One of the interesting takeaways from our research is that ECEM is actually three market segments, not one.

ECEM is the enterprise-wide category, aimed at executives and line-of-business management, helping them to monitor, analyze, and manage carbon emissions and energy consumption across all companies assets and activities.

Closely related but so far distinct from ECEM is operational carbon and energy management (OCEM), which is more narrowly targeted at facility and operations managers and their province of corporate facilities and infrastructure assets (buildings, manufacturing facilities, vehicles, etc.).

And a third set of buyers and asset categories comprise ICT carbon and energy management (ICTCEM) systems, designed to help IT and communications systems management understand and reduce the carbon/energy footprint of ICT assets like data centers and corporate networks.

And in parallel with distinct but related buyer segments, there are three classes of suppliers emerging to address these opportunities (see figure below, and click for full-sized.)

1. ECEM software targeting executive/business levels -- the most crowded segment today.

These solutions are geared to help executive and line-of-business management monitor, analyze and manage carbon emissions, as well as energy consumption, which is their principal source, across operational or functional silos. These systems act as aggregators of energy consumption information coming from various sources, and use embedded carbon calculation methods to automate carbon emission analyses.

Via intelligence and dashboard capabilities, users are able to drill down from a corporate-wide view of carbon and energy information into specific geographies, locations, or asset categories. However, these solutions are typically not able to directly control those assets. Today, we find a highly diverse field of players in this market, where the number of vendors is increasing literally on a weekly basis. Large enterprise software suppliers like CA, SAS, and SAP are vying with EH&S specialists like Enablon and Enviance, and with pure plays like Hara and PE International.

And there are plenty of partnerships forming between these suppliers and with the sustainability practices of consultants like Deloitte, Infosys, and CapGemini.

There are also a number of energy management service providers such as EnerNOC, FirstCarbon Solutions, and Summit Energy, which offer ECEM software, but primary use it as platforms for offering ECEM as a fully-outsourced service. We term this platform-based environmental intelligence and consulting services, which has similarity to platform business process outsourcing (BPO) services.1 Forrester foresees platform-based services as a new trend emerging for both software vendors and service providers to tap into new revenue opportunities, especially with the rising sophistication of platforms and the skills required to leverage them.

2. OCEM software -- the province of large industrial-systems players.

These solutions are primarily proprietary systems that monitor and control energy-intensive systems like heating, ventilating, and air conditioning (HVAC) in facilities. Hence OCEM is primarily used at the facility and operations management level to control and manage the energy usage of distinct facilities or production assets. Therefore, these systems are less integrated with other systems and do not provide sophisticated intelligence and analytics capabilities.

Furthermore, these systems primarily track energy consumption, with little or no focus on carbon emissions. This segment due to its proximity to physical infrastructures is dominated by industrial giants such as GE, Ingersoll Rand, Schneider Electric and Siemens as well as building automation providers such as Honeywell, Johnson Controls, Philips Teletrol, and recently Verizon Business.

In addition, we also include smart grid management solutions in the OCEM category, with providers such as Echelon and Viridity Energy. We have the OCEM market on our research agenda as the next area to do a deeper dive on.

3. ICTCEM software -- characterized by data center and PC power management solutions.

These solutions help IT management monitor and control energy consumption of ICT assets. The focus of the vendors' solutions is primarily on the data center (for example by vendors such as 1E, IBM Big Fix, Sentilla, and SynapSense) and PC (e.g., 1E, Faronics, and Verdiem).2

As in OCEM, these solutions primarily focus on energy usage and typically do not have embedded carbon measurement or reporting functionality. JouleX, a new company that officially launched its business in April this year, introduced an innovative technology that tracks energy consumption of any device connected to the network without using software agents, and translates that into carbon emissions estimates based on location and power source.

As sustainability continues to climb on the corporate strategy agenda of enterprises, the imperative to track, manage, and disclose carbon emissions will become embedded into the nervous system -- and software backbone-- of most companies. We're looking forward to tracking this market as it evolves, and welcome your input and questions.

1. Outsourcers like Accenture, Genpact, Infosys, and Tata Consultancy Services (TCS) are making another run at the BPO market. This new line of attack is based on a standard software "platform" underpinning the BPO offering. No longer will these and other suppliers take over the hodge-podge of client systems in order to run the process. They now offer a full "integrated platform" that includes a standard software offering, not just the people and the process expertise. Forrester believes that including a standard software foundation will cut costs for clients by an additional 20% to 30% on top of the 15% to 20% savings of a traditional BPO solution. See the January 29, 2010, “Platform BPO: Process Outsourcers Take A New Approach To Traditional BPO” Forrester report. [56039]

2. Forty-three percent of companies are implementing PC power management, with another 48% considering it. IT professionals are considering PC power management suites to help overcome common barriers, particularly those affecting user experience, and to determine the level of financial savings, which in turn will help maximize savings. In fact, the Forrester TechRadar™ analysis of green IT 1.0 technologies found that PC power management suites are poised for significant success. Client management suite vendors are the highly preferred supplier of this technology, but standalone solutions should be considered if the vendor does not offer the service or lacks critical functionality. See the August 7, 2009, “PC Power Management Suites Help Overcome Barriers To Maximize Financial Savings” Forrester report. [54947]