The United States is in a golden era for climate policy.

The policy has been a long time coming, yet came to fruition quickly, responding to the urgency of the climate crisis and the opportunity to legislate before midterms.

How the policy will unfold is impossible for me to imagine. What I know: Billions of dollars will flow to research, development and deployment of climate technologies at an unprecedented speed and scale. Meanwhile, geopolitical wildcards — such as supply chain disruptions and the global energy crisis — will throw many curveballs.

As incentives and mandates collide with real-world conditions, there are sure to be pinch points the clean energy sector must navigate. The sooner we anticipate these, the better positioned we will be to address friction.

Catch up fast: Recent climate legislation

The federal government has passed a climate bonanza for the U.S. over the last two months, primarily taking market-based approaches to incentivize clean technologies, deployments and markets. The legislation includes:

- The Inflation Reduction Act (IRA), which will spend roughly $370 billion on decarbonization and climate resilience over the next 10 years and is projected to get the U.S. two-thirds of the way to its emissions goals by 2030.

- The CHIPS and Science Act, a $280 billion bill aimed at revitalizing the American semiconductor industry, with a quarter of that accelerating the growth of zero-carbon industries. That’s more money for climate action than all of the renewable-energy tax credits from 2005 to 2019.

- The Kigali Amendment, which will phase out the world’s use of hydrofluorocarbons, the most significant environmental treaty the U.S. has joined in the last decade.

State and local governments are also getting ambitious, with policies that include more command-and-control approaches:

- California became the first state to require new vehicles sold by 2035 to be zero-emissions — a policy that New York plans to follow.

- A dozen states have adopted clean electricity targets over the last few years, covering areas that comprise more than half of the U.S. population.

- At the local level, 60 cities and counties have restricted natural gas hook-ups in buildings in some capacity, a trend that may accelerate with the flow of new money to all-electric buildings as part of the IRA.

These policy signals are historic and come not a moment too soon. And implementing them will cause short-term turmoil on the way to long-term stability.

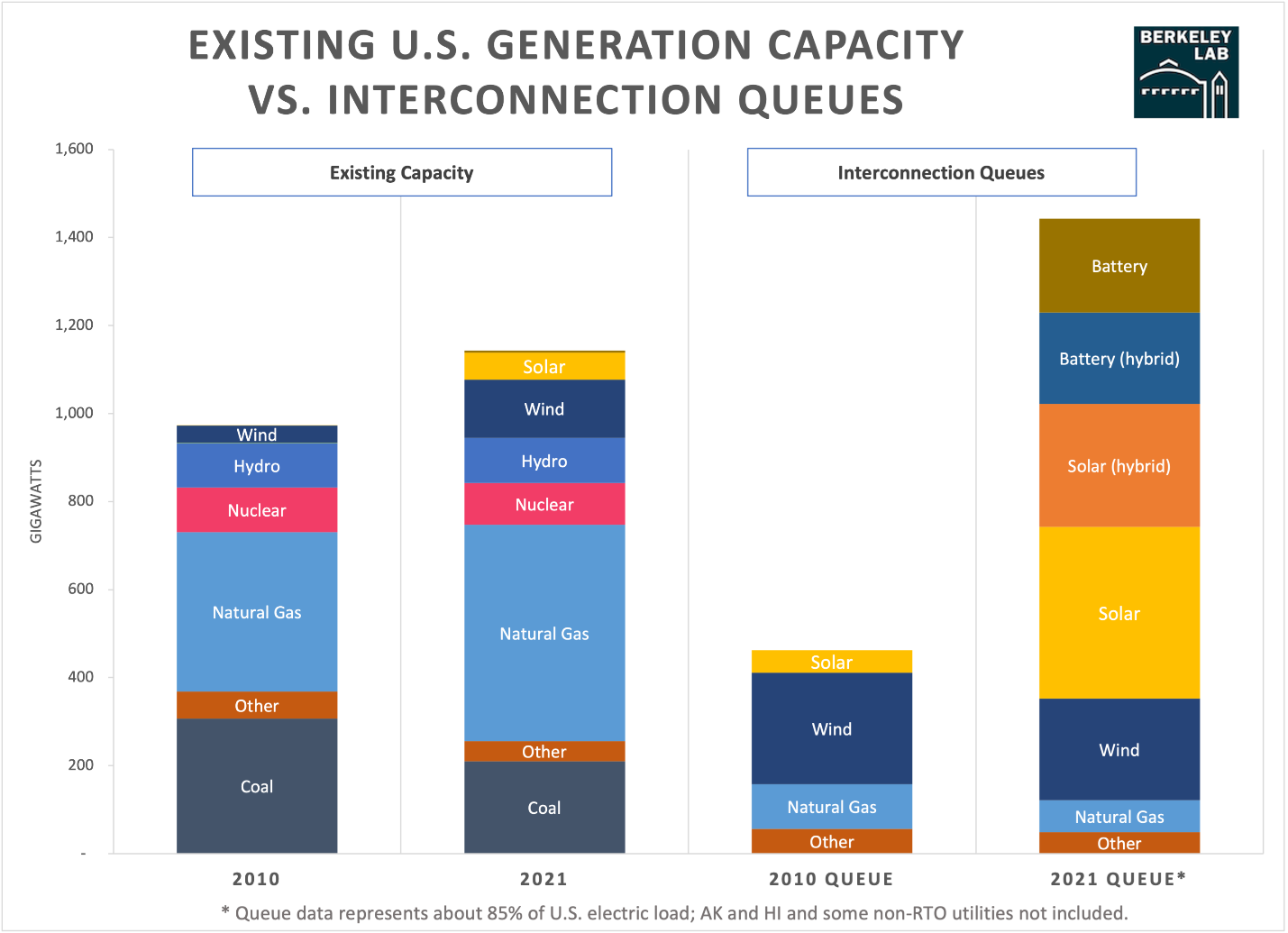

Pinch Point 1: New deployments vs. interconnection delays

When a new energy project wants to connect to the U.S. grid, it must join the interconnection queue to go through a system operator approval process. This queue has been a growing problem for years as new energy projects are getting in line faster than regulators are reviewing them. In 2021, the average wait time for a new project to interconnect was about 3.7 years — up from about 2.1 years from 10 years earlier.

The lag impacts the cost and speed of projects coming online. A study earlier this year from Berkeley Lab showed that enough renewable energy is in the pipeline to bring the U.S. electricity grid to 80 percent carbon free power by 2030. But if the past is a predictor of the future, less than a quarter will be built, thanks to delays in interconnection.

With the new tax credits under the IRA, demand for new projects is set to surge.

Renewable energy developers warn that the challenge is intertwined with permitting delays and congested transmission lines — all of which could affect the speed and scale of deploying new energy projects.

Interconnection delays also threaten the speed of new electric vehicle infrastructure deployment, a looming challenge for companies looking to electrify fleets as well as people who want to go all-electric.

In part, the backup reflects that the process to assess the impacts of new clean energy projects (conducted by transmission system operators) hasn’t caught up to the speed of the energy transition. (The Senate was poised to streamline permitting through legislation, but the provision was dropped because it lacked the votes.)

In order to realize the benefits of clean energy (and their tax incentives), states and localities need to address this regulatory quagmire — hopefully before the logjam grows larger.

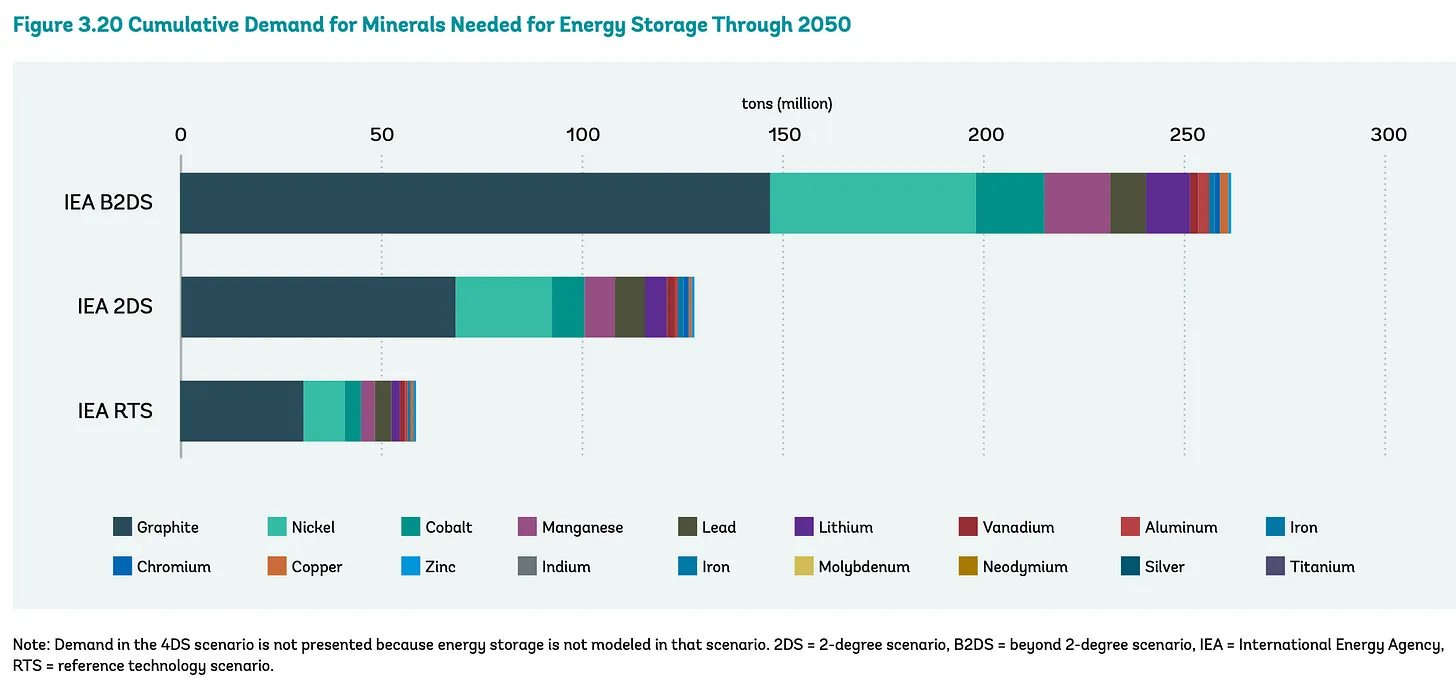

Pinch Point 2: Energy storage demands vs. material sourcing

Demand for energy storage is on the rise. The U.S. energy storage market set a new record in the first quarter of the year, with installations totaling 2.4 gigawatt hours (GWh), according to Wood Mackenzie. By 2026, WoodMac expects the storage markets to grow by nearly 7 GWh annually — a figure that may be conservative given the policy incentives.

It’s not hard to see why: Storage adds energy resilience and reliability on a grid powered by intermittent wind and solar.

The IRA is designed to supercharge demand for energy storage through making it eligible for the same tax benefit (the investment tax credit) that is credited with springboarding the solar industry.

In the long term, increasing energy storage deployments will drive the cost down, per Moore’s Law. In the short term, however, the increased demand — coupled with supply and pricing issues — will reveal the weak links in our sourcing infrastructure.

According to the World Bank, reaching climate goals will require a significant increase in minerals. If the world is to stay under 2 degrees warming, minerals demand from energy storage will double. If the world targets 1.5 degrees, it will more than double again.

The industry’s challenge: Develop the mining practices and supply chains needed to source sufficient minerals for batteries (and other technologies), without negatively affecting the environment or communities where the minerals are.

The IRA aims to address some of the unintended consequences of ramping up energy storage by creating criteria for "qualifying" energy projects in the U.S. tax code, including where and how the technologies are made and sourced. And, according to the World Bank, the world should have plenty of minerals available for this transition.

Pinch Point 3: New clean energy deployments vs. supply chain disruptions

This year, the cost of power purchase agreements did something novel: It increased.

The reason, according to Edison Energy’s Renewables Market Report, is a combination of factors. First, demand is up, as offtakers strive to lock in energy costs and meet clean energy goals. Second, U.S. labor laws and supply chain contrast increased the cost of labor, raw materials and shipping. Third, the Ukraine war and COVID-19 are driving higher costs in contracts. And fourth, interconnection queues are translating into longer project times.

With new tax cuts for more projects, the demand for renewables is sure to increase. That, in term, will put more pressure on supply chains and deployments, which could lead to further project delays.

Once again, in the long term, the clean energy supply chains are bound to strengthen. Much of the federal legislation is designed to shore up U.S. manufacturing in order to streamline supply chains and grow the industry. But in the short term, these factors (along with other wildcards) could create confusion, frustration and friction when it comes to deploying projects.

What else?

As we continue down the road of the great energy transition, there are sure to be many, many more pinch points. I highlight these not to criticize policy or the effort to scale clean technologies but to better understand how companies and customers can prepare.

What other pinch points and disconnects do you see coming as we scale faster than markets organically allow? Where do policy mandates seem impossible because of other regulations? What technologies and supply chains are lagging on the path to meet targets? Let me know: [email protected].